Financing Your Multiplex Purchase

The BoC rate sits at 2.25%. Insured 5-year fixed rates start around 3.94%. CMHC now covers properties up to $1.5M with as little as 5% down. Here's every number you need to finance a multiplex in Greater Vancouver.

Key Topics

Down Payments Demystified

5% on the first $500K, 10% on the rest up to $1.5M. A $750K multiplex needs $50,000 down. A $1M property needs $75,000. Above $1.5M, you're looking at 20% minimum and no CMHC insurance.

Mortgage Rates Right Now

Best 5-year fixed rates sit around 3.94% for insured mortgages. Variable rates start near 3.30–3.35%, tracking below fixed for the first time in a while. The BoC held at 2.25% in March 2026.

Stack Your Down Payment

FHSA: $8K/year tax-deductible, $40K lifetime, tax-free withdrawals. HBP: $60K per person from your RRSP ($120K per couple). Combined, that's up to $200K for a couple — before you touch your savings account.

BC Property Transfer Tax Savings

First-time buyers pay zero PTT on the first $500K of homes up to $835K — saving up to $8,000. Newly built homes get full exemption up to $1.1M. These stack with federal programs.

Rental Income Changes the Math

Lenders count 50–80% of projected rental income toward your qualification. On a duplex with a $2,400/month suite, that's $14,400–$23,040 added to your annual qualifying income. GDS limit: 39%. TDS limit: 44%.

30-Year Amortization Is Real

Since December 15, 2024, all first-time buyers and all buyers of new construction can get 30-year amortization on insured mortgages. That drops monthly payments roughly 10% compared to 25-year terms.

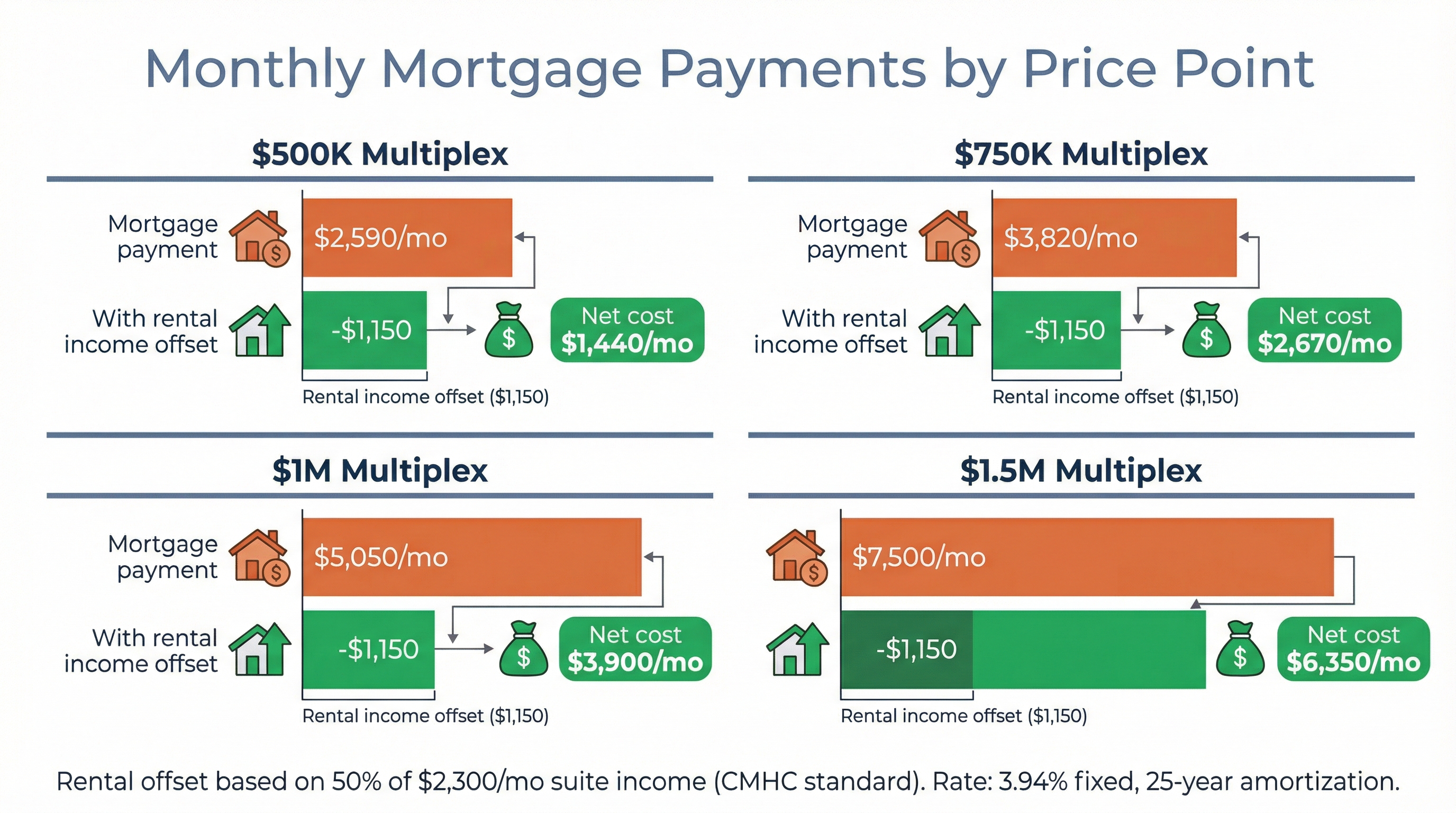

Down Payment & CMHC Insurance Costs

Real numbers at four price points. CMHC premiums are added to your mortgage balance, so you don't pay them upfront — but you do pay interest on them for the life of the loan.

| Purchase Price | Min. Down Payment | Down % | CMHC Premium Rate | CMHC Premium $ | Total Mortgage | Monthly Payment |

|---|---|---|---|---|---|---|

| $500,000 | $25,000 | 5.0% | 4.00% | $19,000 | $494,000 | $2,590 |

| $750,000 | $50,000 | 6.7% | 4.00% | $28,000 | $728,000 | $3,820 |

| $1,000,000 | $75,000 | 7.5% | 4.00% | $37,000 | $962,000 | $5,050 |

| $1,500,000 | $125,000 | 8.3% | 4.00% | $55,000 | $1,430,000 | $7,500 |

Monthly payments based on 3.94% 5-year fixed rate, 25-year amortization. Down payment: 5% of first $500K + 10% of remainder per CMHC rules. CMHC premium at 4.00% (highest tier, 5–9.99% down). At 10% down the premium drops to 3.10%; at 15% down it's 2.80%. Sources: Ratehub.ca best insured rates, March 2026; CMHC premium schedule.

Source: CMHC mortgage loan insurance premium schedule. Premium rates identical across CMHC, Sagen, and Canada Guaranty.

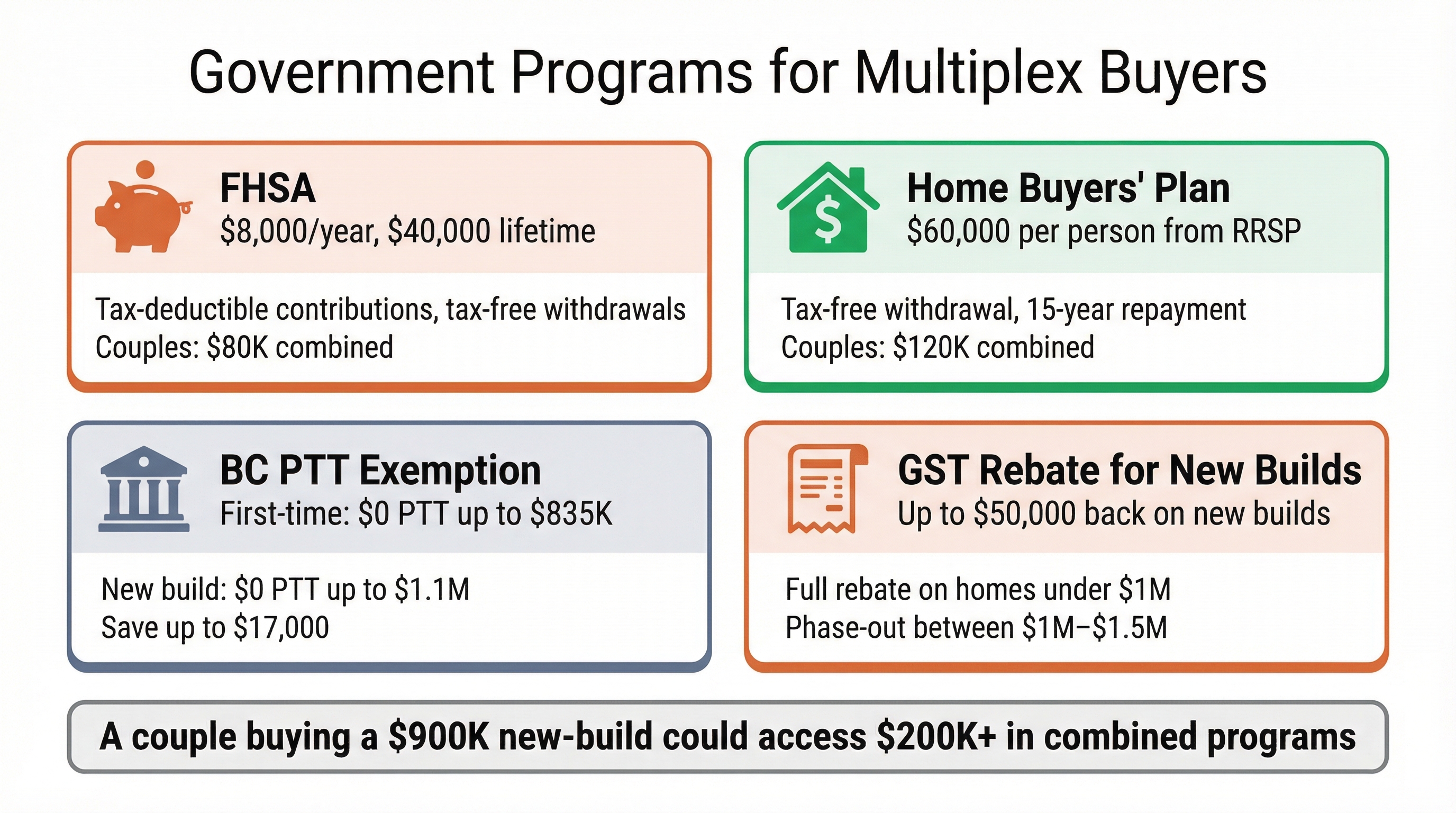

Government Programs at a Glance

Four programs that can save you anywhere from $8,000 to $50,000 on a multiplex purchase. All numbers verified against federal and provincial sources as of March 2026.

First Home Savings Account (FHSA)

Tax-deductible contributions, tax-free growth, and tax-free withdrawals for your first home. Unused room carries forward up to $8K/year — so you can contribute $16K in year two if you missed year one. Couples each open their own FHSA for $80K combined.

Canada.ca — First Home Savings Account

Home Buyers' Plan (HBP)

Withdraw from your RRSP tax-free for a first home. Limit raised from $35K to $60K in April 2024. Repay over 15 years. Temporary relief: withdrawals made between 2022–2025 get an extra 3-year grace period before repayment starts.

Canada.ca — Home Buyers' Plan

BC Property Transfer Tax Exemption

First-time buyers pay zero PTT on the first $500K of a home priced up to $835K. Partial exemption phases out between $835K–$860K. Must have lived in BC for 12 consecutive months or filed 2 tax returns in the last 6 years.

BC Gov — Property Transfer Tax Exemptions

First-Time Buyer GST Rebate (New 2025)

Brand new: eliminates GST on newly built homes up to $1M for first-time buyers. Phases out between $1M–$1.5M. Replaces the old $6,300 max rebate with up to $50,000 back. Applies to purchase agreements signed after May 26, 2025.

Canada.ca — GST Relief for First-Time Home Buyers, May 2025

What stacking looks like for a couple

A couple buying a $900K new-build multiplex unit could bring $200K from FHSA + HBP alone — well above the $65K minimum down payment. Add up to $50K back in GST rebate and $8K in PTT savings. These programs are designed to stack.

How Rental Income Changes Your Qualification

This is where multiplexes pull ahead. Lenders count a portion of projected rental income toward your debt service ratios — which means you qualify for a larger mortgage than you would buying a condo or a house.

Without Rental Income

With Duplex Rental Income

Gross Debt Service. Your housing costs (mortgage, taxes, heat, half of strata fees) can't exceed 39% of gross income. This is the CMHC maximum for insured mortgages.

Total Debt Service. All debts (housing + car payments, credit cards, student loans) can't exceed 44% of gross income. Lenders stress-test at the higher of your rate +2% or 5.25%.

Rental income offset varies: most lenders use 50% of gross rent; some allow up to 80% or use a full offset method (100% of rent minus 100% of costs). OSFI's 2025 guidance prohibits double-counting income across multiple properties. Sources: CMHC debt service guidelines; OSFI B-20 rental income clarification, September 2025.

25 vs. 30-Year Amortization

Since December 15, 2024, all first-time buyers and all new construction buyers can choose 30-year amortization on insured mortgages. Here's what that looks like on an actual multiplex purchase.

| Mortgage Amount | 25-Year Monthly | 30-Year Monthly | Monthly Savings |

|---|---|---|---|

| $500,000 | $2,620 | $2,370 | $250 |

| $700,000 | $3,670 | $3,320 | $350 |

| $900,000 | $4,720 | $4,270 | $450 |

| $1,200,000 | $6,290 | $5,690 | $600 |

Based on 3.94% 5-year fixed rate. The trade-off: 30-year amortization means slower equity building and roughly 15–20% more total interest over the life of the mortgage. Source: Ratehub.ca, March 2026; Ratehub.ca amortization comparison.

The bottom line

The financing environment for multiplex buyers is the best it's been in years. The Bank of Canada cut from 5.00% down to 2.25% through 2024-2025, and variable-rate mortgages are pricing below fixed for the first time in a while — around 3.30% vs. 3.94% fixed. On a $700K mortgage, that difference puts real money back in your pocket every month.

The qualification math works harder for multiplex buyers than any other housing type. CMHC's rental income offset means lenders count 50% of projected suite income toward your application. A couple earning $130K with no other debts qualifies for roughly $585K-$695K depending on rental income — enough for a multiplex unit in Surrey, Burnaby, or East Vancouver. The stress test at 5.94% keeps you safely within your means.

The government programs are stacking up in your favour. FHSA + HBP can get a couple to $200K in down payment funds. The GST rebate delivers up to $50K back on new builds. FHSA contributions max at $8K/year and HBP draws from your existing RRSP — so start early and let those programs compound. The earlier you begin, the stronger your position at closing.

For first-time multiplex buyers, the path is clear: rates are favourable, programs are generous, and CMHC insurance on properties up to $1.5M means you can get in with as little as 5% down. OSFI's 2025 guidance on income qualification is worth understanding, but it doesn't change the math for a first purchase — it mainly affects portfolio investors.

Every month you wait, you're leaving government incentives and favourable rates on the table. Explore the full Playbook for more guides, or talk to our team to get matched with a mortgage broker who specializes in multiplex financing.

Data: Bank of Canada policy rate decisions, March 2026. Ratehub.ca best mortgage rates, March 2026. CMHC insured mortgage rules, December 2024. Canada.ca FHSA and HBP program details. OSFI B-20 rental income guidance, September 2025.

Key Takeaways

- Multiplexes up to $1.5M qualify for CMHC-insured mortgages with as little as 5% down.

- Lenders can count up to 50% of projected rental income to boost your qualifying amount.

- The FHSA lets first-time buyers save up to $40,000 tax-free toward a down payment.

- BC's new housing programs offer forgivable loans and exemptions specifically for multiplex buyers.

- 30-year amortization is now available for first-time buyers, lowering monthly payments by roughly 10%.

- Stacking federal and provincial programs can reduce your upfront cash requirement by $50,000 or more.

Frequently Asked Questions

What is the minimum down payment for a multiplex in Canada?

For multiplexes up to $999,999, the minimum is 5% on the first $500,000 and 10% on the remainder. Properties between $1M and $1.5M now qualify for insured mortgages with the same tiered structure under updated CMHC rules effective December 2024.

Here is what the numbers look like in practice. On a $750K multiplex, your minimum down payment is $50,000 (5% of $500K plus 10% of $250K). On a $1M property, it is $75,000. The December 2024 CMHC rule change was significant — previously, anything over $999,999 required 20% down, which meant $200K on a million-dollar property. Now that same purchase needs only $75K. The trade-off is you will pay a CMHC insurance premium (around 4% of the mortgage amount at minimum down), which gets added to your mortgage balance. On a $750K purchase with $50K down, that premium is roughly $28,000. You pay interest on it for the life of the loan, so the true cost is higher than the premium alone.

Can rental income help me qualify for a mortgage?

Yes. Most lenders allow you to add 50% of projected rental income from secondary suites to your gross income when qualifying. This can significantly increase your purchasing power, sometimes by $100,000 or more depending on local rent levels.

The way it works: your mortgage broker submits an appraisal or rental market analysis showing the expected rent for your secondary suite. Most lenders use 50% of that projected income (some use up to 80% with strong documentation) and add it to your gross household income for qualification purposes. For example, if a secondary suite in your target area rents for $2,300 per month, a lender using the 50% rule would add $1,150 monthly — or $13,800 annually — to your qualifying income. At current rates, that can translate to roughly $80K-$120K in additional borrowing capacity. The key is having realistic rent projections backed by comparable listings. Ask your broker which lenders have the most favourable rental offset policies, as this varies significantly between institutions.

What is the FHSA and how does it help homebuyers?

The First Home Savings Account (FHSA) lets first-time buyers contribute up to $8,000 per year, to a lifetime maximum of $40,000. Contributions are tax-deductible and withdrawals for a qualifying home purchase are completely tax-free.

The FHSA is effectively a hybrid of an RRSP and a TFSA designed specifically for first-time homebuyers. Your contributions reduce your taxable income in the year you make them (like an RRSP), and when you withdraw for a qualifying home purchase, there is zero tax on the withdrawal or any investment gains (like a TFSA). You can carry forward up to $8,000 of unused contribution room to the following year, so if you miss a year you can contribute $16,000 the next. The account must be open for at least one year before you can make a qualifying withdrawal. You can also combine the FHSA with the Home Buyers' Plan, withdrawing up to $60,000 from your RRSP — giving you access to $100,000 in tax-advantaged down payment funds if you have maximized both programs.

What government programs help multiplex buyers in BC?

BC offers the First-Time Home Buyers' Program (property transfer tax exemption up to $835,000), the BC Home Owner Mortgage and Equity Partnership, and federal programs like the Home Buyers' Plan ($60,000 RRSP withdrawal) and the FHSA.

Stack these programs strategically for maximum benefit. The BC First-Time Home Buyers' Program exempts you from Property Transfer Tax on purchases up to $835K (partial exemption to $860K) — that saves you up to $13,500 in closing costs. The federal Home Buyers' Plan lets you withdraw up to $60,000 from your RRSP tax-free for a down payment, with 15 years to repay it. Combine that with an FHSA for up to $40,000 more. On new builds, the GST New Housing Rebate returns up to $6,300 of the 5% GST. First-time buyers also get 30-year amortization on new builds (versus the standard 25), which lowers monthly payments by roughly 8-10%. Talk to a mortgage broker who specializes in multiplex purchases — they will know which programs you qualify for and how to layer them effectively.

Can I really use rental income to qualify for a bigger mortgage?

Yes, but the math is more conservative than you might expect. Most lenders count only 50% of projected rental income toward your qualification. On a $2,300/month suite, that adds $1,150/month — roughly $80K-$120K in extra borrowing power at current rates.

Here is how it works in practice. Your mortgage broker orders an appraisal or provides a rental market analysis showing expected rents for the secondary suite. The lender takes 50% of that figure and adds it to your gross household income for GDS/TDS ratio calculations. Some credit unions and monoline lenders will use up to 80% with strong documentation, but the Big Five banks generally stick to 50%. CMHC-insured mortgages follow the same 50% offset rule. The catch is that the rental income must be realistic and supported by comparable listings in the area — you cannot inflate the number. Also, not every lender treats rental income the same way. Some require a signed lease, others accept market estimates. Ask your broker specifically which lenders have the most favourable rental offset policies, because the difference between 50% and 80% offset can mean $40K-$60K in additional qualification room.

Is house-hacking a multiplex actually worth the hassle?

For most buyers under 40, yes — but go in with open eyes. The rental income is real ($2,000-$3,000/month on a duplex suite), but so is the landlord workload: tenant screening, maintenance calls, and navigating the BC Residential Tenancy Act.

The financial case is strong. Living in one unit of a duplex and renting the other can cut your effective housing cost by 30-50%. On a $900K duplex with a $4,200/month mortgage, a $2,500/month rental suite drops your net cost to $1,700. That is less than renting a one-bedroom in many parts of Vancouver. The downsides are real though. You are now a landlord under BC law, which means you must follow the Residential Tenancy Act for everything — rent increases capped at 2.3% in 2026, 4-month notice for landlord-use eviction, and mandatory use of the RTB portal for all notices. You will field maintenance calls at inconvenient times. Your tenant's noise is your noise. And the tax complexity is significant: you must declare rental income, can deduct a portion of mortgage interest and expenses, and may face capital gains implications on the rental portion when you sell. For people who are handy, organized, and comfortable setting boundaries with neighbours, house-hacking is one of the best wealth-building strategies available in Vancouver. For people who value total privacy and hate administrative work, a condo might be the better call.

Financing Articles

House Hacking a Multiplex

Live in one unit, rent the rest — cash flow math, tax implications, and landlord reality.

Co-Development Explained

How the money works when you partner with a developer — land equity, construction financing, and take-out mortgages.

More from The Playbook

Why Multiplex

The case for ground-oriented living

ExploreBuying Guide

From discovery to closing

ExploreMarket Reports

Data, trends & analysis

ExploreLiving

What ownership looks like

ExploreMulti-Gen

Families buying together

ExploreWhere to Buy (Van)

Vancouver neighbourhood data

ExploreWhere to Buy (Burnaby)

Burnaby neighbourhood data

ExploreTalk to a Multiplex Expert

Whether you're buying, building, or exploring your options — our team can help you navigate the process with confidence.

Ready to find your multiplex?

Browse duplexes, triplexes, and fourplexes across Greater Vancouver and BC.