House Hacking a Multiplex: The Honest Guide

Live in one unit, rent the others, and let your tenants cover most of the mortgage. In Metro Vancouver, a 2BR suite rents for $2,363/month on average. That's real money off your housing costs every single month. But you're also signing up to be a landlord — and nobody on Reddit will let you forget what that actually means.

Key Topics

The Cash Flow Math

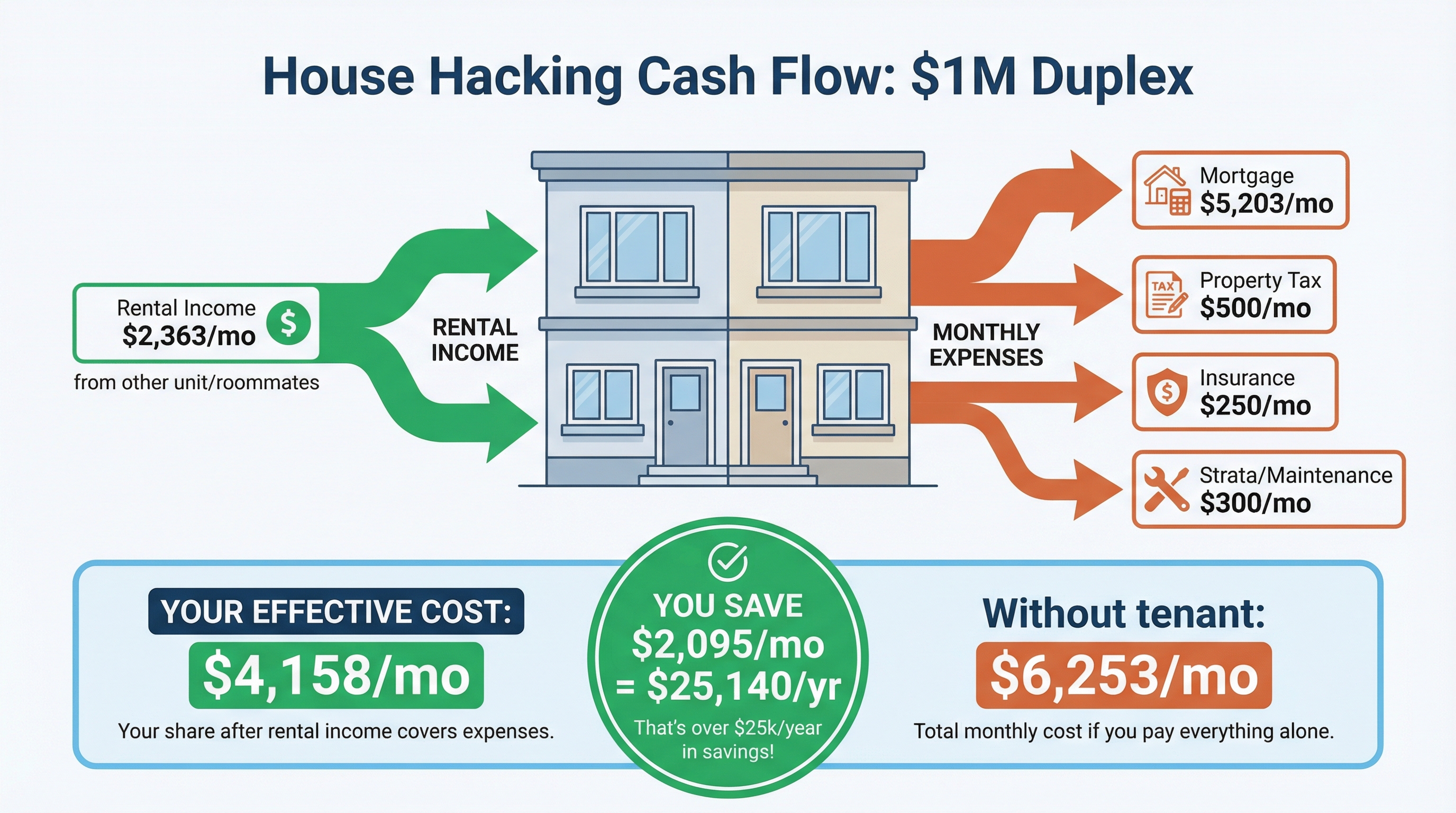

A $1M duplex with 10% down and a tenant paying $2,363/month means your effective housing cost drops to roughly $2,800/month — compared to $5,100/month for a $710K condo with zero income. We run the real numbers below.

Tax Implications You Can't Ignore

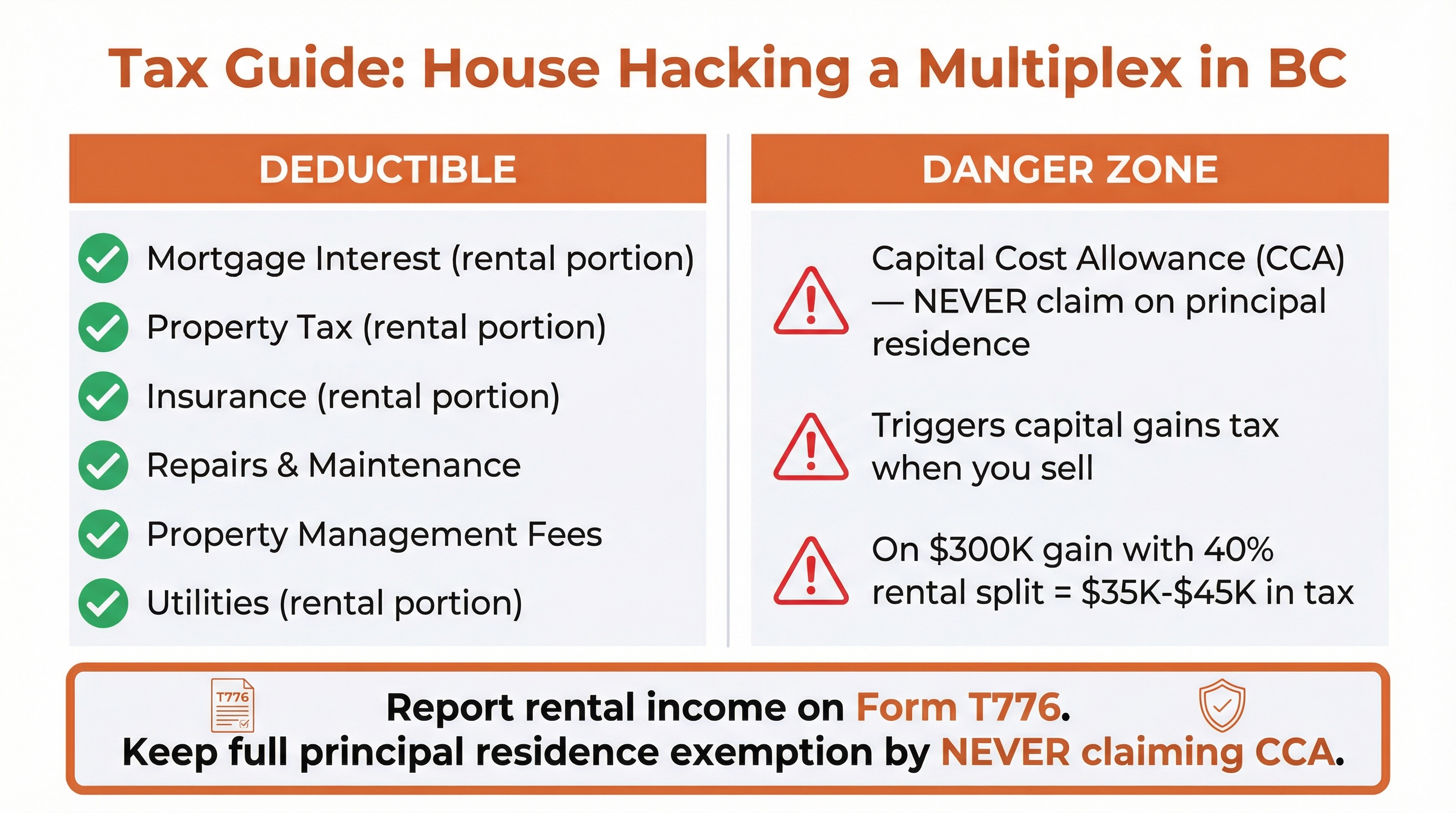

Rental income goes on your T776. You can deduct the rental portion of mortgage interest, insurance, and repairs. But claim CCA on your principal residence and you'll trigger capital gains when you sell. The CRA is watching.

BC Landlord Law Crash Course

Rent increase cap is 3% in 2025, dropping to 2.3% in 2026. Security deposits max out at half a month's rent. Eviction for personal use requires 3 months notice and 12 months occupancy after. The RTB doesn't mess around.

CMHC Qualification Boost

Lenders can count up to 100% of rental suite income toward your mortgage qualification for owner-occupied properties. That extra $2,363/month could increase your buying power by $100K+ when you apply.

The Landlord Reality

Midnight plumbing calls, RTB disputes that drag on for weeks, tenants who looked perfect on paper. House hacking isn't passive income — it's a second job. A well-paid one if you do it right, but a job nonetheless.

Reddit's Collected Wisdom

We compiled the most common advice from r/PersonalFinanceCanada and r/canadahousing: screen tenants like your financial life depends on it (it does), budget for vacancies, and never skip landlord insurance.

Cash Flow: Duplex vs. Condo

Same buyer, same income, two different properties. A $1M duplex with a rental suite vs. a $710K condo with no income. Look at the monthly cost difference.

| Monthly Item | $1M Duplex (Owner-Occupied) | $710K Condo |

|---|---|---|

| Purchase Price | $1,000,000 | $710,000 |

| Down Payment (10%) | $100,000 | $71,000 |

| Mortgage Payment (3.94%, 25yr) | $5,203/mo | $3,694/mo |

| Property Tax | $500/mo | $250/mo |

| Insurance (landlord vs. home) | $250/mo | $100/mo |

| Strata / Maintenance Reserve | $300/mo | $550/mo |

| Total Monthly Costs | $6,253/mo | $4,594/mo |

| Rental Income (2BR suite) | -$2,363/mo | $0 |

| Vacancy Reserve (5%) | +$118/mo | $0 |

| Maintenance Reserve (tenant unit) | +$150/mo | $0 |

| Your Effective Monthly Cost | $4,158/mo | $4,594/mo |

Assumptions: 3.94% 5-year fixed rate (Ratehub, March 2026), 25-year amortization, CMHC-insured. Rent based on CMHC 2025 avg. 2BR purpose-built rent in Vancouver. Property tax estimated from City of Vancouver 2025 rates. This is illustrative -- your numbers will differ.

Tax Implications: What's Deductible, What's Not

You report rental income on Form T776. But one wrong move with CCA can cost you tens of thousands when you sell. Here's the breakdown.

You Can Deduct (Rental Portion)

- Mortgage interest (not principal) -- proportional to rental square footage

- Property tax -- same proportional split

- Insurance premiums for the rental unit

- Repairs and maintenance on the rental unit

- Utilities you pay that serve the rental unit

- Advertising costs for finding tenants

- Property management fees (8-10% of rent in Metro Vancouver)

- Legal and accounting fees related to rental activity

Danger Zone

- CCA (Capital Cost Allowance) -- saves you $1,500-$2,400/yr in tax but KILLS your principal residence exemption

- Mortgage principal payments -- not deductible, ever

- Personal-use portion of any shared expense

- Value of your own labour on the property

- Expenses that create a rental loss if you claim CCA

The CCA Trap: On a property that appreciates $300K with a 40% rental split, claiming CCA could cost you $35,000-$45,000 in capital gains tax at sale. Every experienced accountant says the same thing: skip CCA on your principal residence.

Sources: CRA Form T776 guidelines. Income Tax Folio S1-F3-C2 (Principal Residence). Capital gains inclusion rate: 50% on first $250K, 66.7% above (since June 2024).

The Landlord Reality Check

The cash flow math looks great on paper. Here's what the spreadsheet doesn't tell you about being a landlord who lives in the same building.

Midnight Plumbing Calls

When the toilet in the rental unit backs up at 2 AM, your tenant isn't calling a property management company. They're knocking on your door. You live there. Emergency plumbing in Vancouver runs $200-$500 after hours. Budget for it.

RTB Disputes Take Weeks

If a tenant stops paying rent, you issue a 10-day notice. They have 5 days to pay or dispute. If they dispute, you wait for an RTB hearing -- expedited cases target 6-12 days, standard cases can drag on much longer. Meanwhile, zero rent coming in.

Tenant Screening Is Everything

Credit check, employment verification, references, previous landlord calls. Skip any of these and you're gambling. The tenant who 'seemed great' but smokes through the vents or plays music at midnight is the story every house hacker tells eventually.

Vacancy Costs Add Up Fast

Metro Vancouver's vacancy rate hit 3.7% in October 2025 -- highest since 1988. New buildings are offering 1-2 months free rent to attract tenants. Budget for 2-3 weeks of vacancy per year, plus cleaning and minor repairs between tenants.

You Can't Just Raise Rent

BC caps rent increases at 2.3% for 2026 (3% in 2025). If you underpriced the unit at lease signing, you're stuck with small annual bumps. The only way to reset to market rate is when a tenant voluntarily leaves. No renovictions allowed.

The Boundary Problem

Your tenant knows exactly when you leave for work and when you're home. Some will text you about minor issues constantly. Others will knock on your door to 'chat.' Setting clear boundaries from day one isn't optional -- it's survival.

Sources: CMHC Rental Market Report Oct 2025 (vacancy rate). BC Residential Tenancy Act (notice periods, rent caps). RTB expedited hearing guidelines.

What House Hackers Actually Say

Compiled from r/PersonalFinanceCanada, r/canadahousing, BiggerPockets Canada forums, and Canadian Money Forum. These are the patterns that come up over and over.

What They Wish They Knew

- •"The rental income doesn't cover as much as you think once you account for taxes on that income, maintenance, and vacancy."

- •"Get landlord insurance from day one. My homeowner policy explicitly excluded rental activity and I didn't know until I needed it."

- •"You're not just buying a home, you're starting a small business. Treat it that way -- separate bank account, proper records, read the RTA."

- •"The mortgage offset is real but the stress is also real. It took me a year to stop dreading every text from my tenant."

Biggest Mistakes They Made

- •"Skipped the credit check because the tenant 'seemed nice.' They stopped paying in month 3. It took 4 months to resolve through the RTB."

- •"Claimed CCA on my taxes for 3 years. Accountant told me I'd owe $20K+ in capital gains when I sell. Wish I'd known earlier."

- •"Didn't soundproof between units. I could hear everything. My tenant could hear everything. It was awful for both of us."

- •"Set rent $200 below market to fill the unit fast. With BC's 2-3% annual cap, it took 4 years to get back to market rate."

Best Advice They Give

- •"Screen tenants like your financial life depends on it. Because it does. Credit check, employment letter, call the previous landlord."

- •"Keep 3-6 months of mortgage payments in reserve. One bad tenant or one major repair shouldn't bankrupt you."

- •"Read the BC Residential Tenancy Act cover to cover before your first tenant moves in. Know your rights AND your obligations."

- •"The best house hack is a property where you'd be happy living even if the rental unit sat empty. Don't overextend on the math."

Compiled from r/PersonalFinanceCanada, r/canadahousing, BiggerPockets Canada forums, and Canadian Money Forum discussions (2023-2025). Quotes are paraphrased and condensed for clarity.

BC Landlord Rules: Quick Reference

The Residential Tenancy Act applies to every landlord in BC, including owner-occupiers. Ignorance is not a defence at the RTB.

| Rule | What the Law Says | What It Means for You |

|---|---|---|

| Rent Increase Cap (2025) | 3.0% maximum | You can only raise rent once per year, with 3 full months notice |

| Rent Increase Cap (2026) | 2.3% maximum | Even less room to catch up if you underpriced at lease signing |

| Security Deposit | Max half month's rent | On a $2,363/mo unit, that's $1,181. Pet deposit is another half month |

| Eviction (Personal Use) | 3 months written notice | Must use Landlord Use Portal. Must occupy for 12 months after or owe up to 12 months rent |

| Eviction (Non-Payment) | 10-day notice | Tenant has 5 days to pay in full or dispute. If they pay, notice is cancelled |

| Entry Notice | 24 hours written notice | You can't just pop over because you live next door. Written notice, every time |

| Fixed-Term Leases | Auto-convert to month-to-month | You can't use lease expiry to force a tenant out. Period. |

| Deposit Return | 15 days after tenancy ends | Return deposit or file RTB claim within 15 days, or you forfeit it entirely |

Sources: BC Residential Tenancy Act. BC Gov rent increase announcements (2025, 2026). RTB Information Sheet RTB-114. Personal use eviction rules updated 2024.

The bottom line

House hacking is active ownership — tenant screening, maintenance, RTB paperwork, and tax planning all come with the territory. But that hands-on involvement is exactly what makes it one of the most powerful wealth-building strategies available to first-time buyers in Metro Vancouver.

The math speaks for itself. In a city where a modest condo costs $710K and a detached home is $1.88M, a duplex that lets you live in one unit while a tenant covers $2,000+ of your monthly costs is one of the few realistic paths to homeownership that doesn't require a $200K household income or a family gift for the down payment.

The buyers who thrive treat it like a business from day one. Separate bank account. Proper insurance ($3,600/yr). Thorough tenant screening. A reserve fund for vacancies and the $2,000-$5,000 in annual maintenance. They read the RTA before signing their first lease, skip the CCA deduction to protect their principal residence exemption, and set clear boundaries with tenants. This is a learnable skill set — and the payoff is significant.

House hacking a multiplex in BC is one of the best financial moves available to most first-time buyers right now. Explore the rest of our Playbook to keep building your knowledge, or talk to our team to start running the numbers for your situation. We walk buyers through this every week.

Data: CMHC Rental Market Report 2025, REBGV MLS HPI Dec 2025, CRA Income Tax Folio S1-F3-C2, BC Residential Tenancy Act, Ratehub mortgage rates March 2026.

Key Takeaways

- A duplex owner-occupier can reduce effective housing costs by $2,000+/month vs. buying a condo with no rental income.

- CMHC now allows 100% of rental suite income toward mortgage qualification for owner-occupied properties.

- Never claim CCA on your principal residence -- it triggers capital gains tax when you sell.

- BC rent increase cap drops to 2.3% in 2026; security deposits capped at half a month's rent.

- Budget for 5% vacancy and $2,000-$5,000/year in unexpected maintenance as a landlord.

- Property management runs 8-10% of rent in Metro Vancouver -- worth it once you're tired of tenant calls.

Frequently Asked Questions

How much can you save by house hacking a duplex in Vancouver?

On a $1M duplex with 10% down, renting the second unit at $2,363/month drops your effective housing cost from roughly $5,200/month to about $2,800/month. That's $28,800 per year in savings compared to carrying the full mortgage alone.

The exact savings depend on your purchase price, down payment, interest rate, and local rental rates. A fourplex owner-occupier renting out three units could potentially cover the entire mortgage and pocket cash flow on top. But the numbers need to account for real costs: property tax ($4,000-$8,000/year in Vancouver), insurance ($1,800-$3,600/year for landlord coverage), maintenance reserve (budget 1% of property value annually), and vacancy gaps. The 3.7% vacancy rate in Metro Vancouver as of October 2025 means you should expect roughly two weeks of vacancy per year per unit.

Does CMHC count rental income when qualifying for a mortgage?

Yes. For owner-occupied properties with a legal rental suite, CMHC now allows lenders to count up to 100% of net rental income toward your debt service ratios. Previously the limit was 50%. This can boost your purchasing power by $100K or more.

The rental suite must have a separate entrance and comply with local zoning requirements. Your lender will want to see a signed lease or a professional appraisal estimating market rent. Starting in 2026, mortgages where rental income exceeds 50% of qualifying income will be classified as 'income-producing residential real estate' (IPRRE), which carries higher capital requirements for banks. This could mean slightly higher rates for heavily rental-dependent applications. For most duplex owner-occupiers, the rental income will be well under 50% of total qualifying income, so this rule likely won't apply.

What are the tax implications of renting part of your home in Canada?

You report rental income on Form T776 and can deduct the rental portion of expenses like mortgage interest, property tax, and insurance. The CRA allows you to keep the full principal residence exemption as long as you don't claim CCA and the rental use is secondary.

The CRA's position is that if the rental portion is relatively small compared to your personal use, you don't make structural changes specifically for renting, and you never claim Capital Cost Allowance (CCA), the entire property can still qualify for the principal residence exemption when you sell. CCA is the trap most new landlords fall into: claiming $5,000-$8,000/year in depreciation saves you maybe $1,500-$2,400 in tax, but it triggers a deemed disposition and partial capital gains when you sell. On a property that appreciated $300,000, that mistake could cost you $30,000+ in tax. Every accountant who works with rental properties will tell you the same thing: skip the CCA on your principal residence.

What are BC's rules for landlords who live in their own building?

BC's Residential Tenancy Act applies equally whether you live in the building or not. Rent increases are capped at 2.3% for 2026, security deposits max at half a month's rent, and personal-use eviction requires 3 months notice plus 12 months of occupancy after.

Living in the building doesn't give you special landlord powers under BC law. You still need to go through the Residential Tenancy Branch for disputes, follow the same notice periods, and respect tenant privacy with 24 hours written notice before entering. Fixed-term leases automatically convert to month-to-month in BC -- you can't use lease expiry as a de facto eviction. For personal-use evictions, you must now use the Landlord Use Portal, and if you don't actually move in and stay for 12 months, the tenant can claim compensation of up to 12 months' rent. The RTB handles disputes through hearings that can take weeks to schedule, though expedited hearings for urgent matters target 6-12 days.

How much does landlord insurance cost in BC?

Landlord insurance in BC starts around $40/month ($480/year) for basic coverage, but most multiplex owners pay $150-$300/month for comprehensive policies. That's roughly 25% more than standard homeowner insurance and covers liability up to $1-2M.

Standard homeowner insurance does NOT cover rental activities. If a tenant's guest slips on your front steps and you only have homeowner insurance, you could be personally liable. Landlord insurance typically covers the building structure, liability claims, loss of rental income during repairs, and legal costs from tenant disputes. Some policies also cover tenant-caused damage beyond normal wear and tear. Get quotes from Square One, BCAA, and local brokers. The cost depends on property age, location, coverage limits, and your claims history. Budget $2,400-$3,600/year for a duplex in Metro Vancouver with $2M liability coverage.

What happens to my principal residence exemption if I sell a house-hacked property?

If you never claimed CCA and the rental portion was secondary to your personal use, the CRA typically allows the full principal residence exemption. Claim CCA even once, and you'll owe capital gains tax on the rental portion when you sell.

The CRA's Income Tax Folio S1-F3-C2 lays this out clearly. When you sell a property that was partially rented, you technically need to split the gain between the personal-use portion (exempt) and the rental portion (taxable). But the CRA's longstanding administrative practice is to waive this split if three conditions are met: the rental use was ancillary to your personal use, you made no structural changes for the rental, and you never claimed CCA. In 2024, Canada increased the capital gains inclusion rate to two-thirds for gains over $250,000. On a $400,000 gain with a 40% rental split, you'd owe tax on roughly $106,000 of income. That's $35,000-$45,000 in tax depending on your bracket. Avoiding CCA is the single most important tax decision for house hackers.

More from The Playbook

Why Multiplex

The case for ground-oriented living

ExploreBuying Guide

From discovery to closing

ExploreFinancing

Mortgages, programs & more

ExploreMarket Reports

Data, trends & analysis

ExploreLiving

What ownership looks like

ExploreMulti-Gen

Families buying together

ExploreWhere to Buy (Van)

Vancouver neighbourhood data

ExploreWhere to Buy (Burnaby)

Burnaby neighbourhood data

ExploreTalk to a Multiplex Expert

Whether you're buying, building, or exploring your options — our team can help you navigate the process with confidence.

Ready to find your multiplex?

Browse duplexes, triplexes, and fourplexes across Greater Vancouver and BC.