Your Complete Multiplex Buying Guide

A multiplex gives you more space, lower strata fees, rental income to offset your mortgage, and land ownership in one of the world's most supply-constrained markets. Bill 44 just unlocked the supply. Here's how to move on it — every step from pre-approval to keys, with real numbers.

Key Topics

Pre-Approval Unlocks Rental Income

CMHC allows lenders to count 50% of projected rental income from non-owner units toward your qualifying income. On a fourplex with three rentals at $2,363/month average, that's $3,545/month added to your application. Get pre-approved with a broker who understands multiplex underwriting — not all do.

The Best Inventory Is New-Build

Bill 44 (June 2024) created an entire new category of ground-oriented supply in Metro Vancouver. New-build multiplexes in Renfrew, Mount Pleasant, Burnaby Heights, and Edmonds are listed first on MultiLiving.ca. These units come with PTT exemptions, full warranties, and no deferred maintenance.

Strata Documents Are Your Due Diligence Edge

A small strata means you can actually read every document. The Form B shows the reserve fund, bylaws, and pending issues. On a 4-unit building you can understand the full financial picture in an afternoon — something impossible in a 300-unit tower. This transparency is a feature, not a burden.

New Builds Come Pre-Protected

Every new multiplex in BC carries a mandatory 2-5-10 warranty: 2 years on labour and materials, 5 on the building envelope, 10 on structure. You're not buying someone else's deferred maintenance. BC Housing backs the warranty even if the builder goes under. That's real downside protection.

New Builds Cut Your Closing Costs in Half

A $950K pre-sale multiplex unit pays $0 PTT under the newly built home exemption (up to $1.1M). The same purchase on resale costs $17,000 in PTT. Add the GST New Housing Rebate (up to $6,300 back for owner-occupiers) and new-build closing costs are significantly lower than resale.

The Land Appreciates With You

Unlike a condo, a multiplex unit sits on land. In Metro Vancouver, land value drives long-term appreciation — and land in established neighbourhoods doesn't stay cheap. You're not buying a depreciating concrete box in the sky. You own a share of ground in one of the most supply-constrained markets in North America.

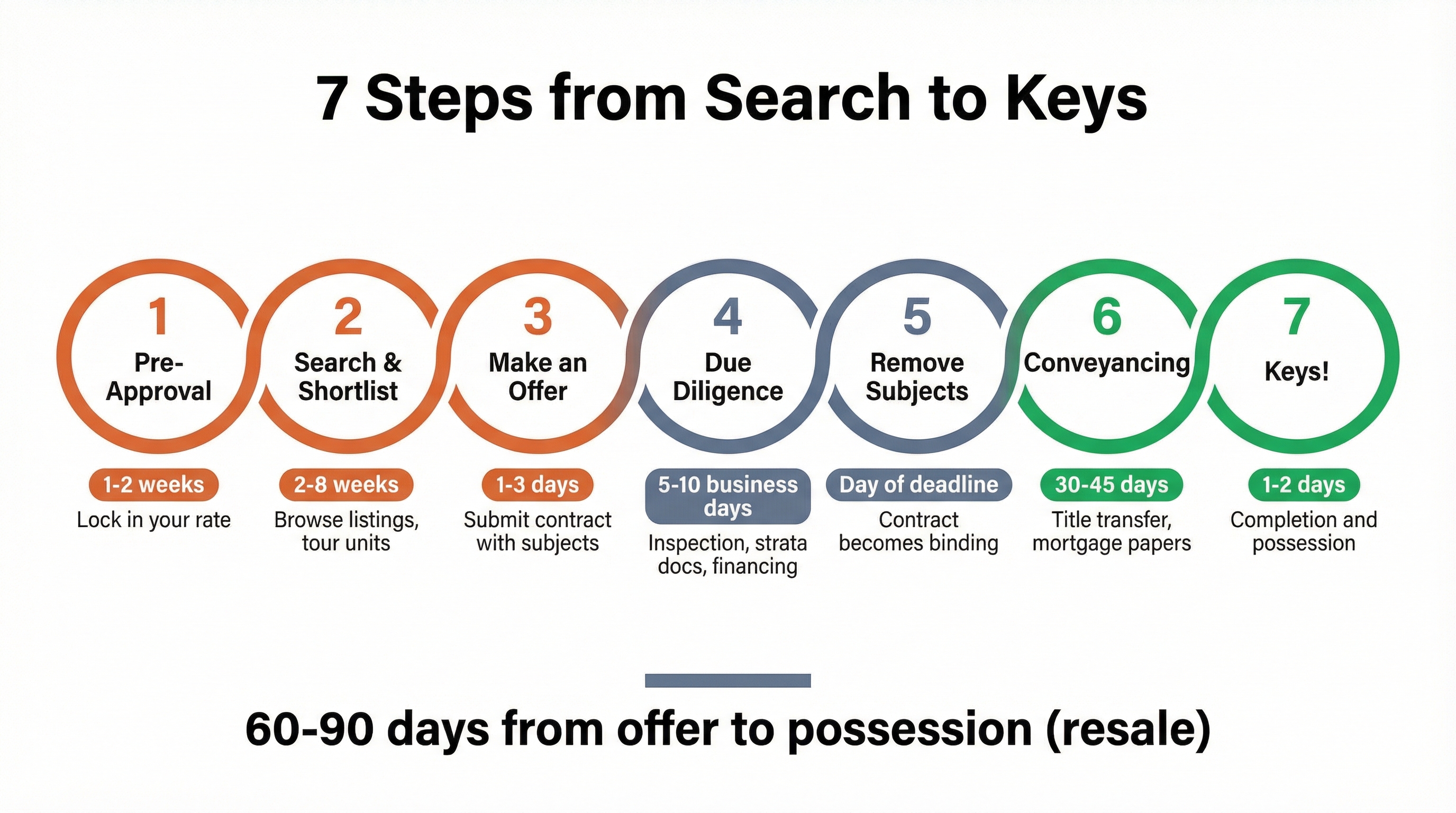

7 Steps from Search to Keys

A resale multiplex purchase in BC typically takes 60-90 days from accepted offer to possession. Pre-sales follow a different timeline entirely — see the comparison below.

Mortgage Pre-Approval

1-2 weeksGather income docs, pull your credit score, and talk to a broker. Pre-approval locks in your rate (typically 90-120 days) and tells sellers you are a real buyer. As of March 2026, the Bank of Canada overnight rate is 2.25%, with 5-year fixed rates around 3.94% insured and variable rates around 3.35%.

Search & Shortlist Properties

2-8 weeksBrowse listings on MultiLiving.ca, attend open houses, tour model suites for pre-sales. Focus on neighbourhood, unit size, rental income potential, and developer reputation. Keep a spreadsheet — you will forget details fast once you have seen five places.

Make an Offer

1-3 daysFor resale: submit a Contract of Purchase and Sale with subjects (financing, inspection, strata review). BC's Home Buyer Rescission Period gives you 3 business days to back out, but exercising it costs 0.25% of the purchase price. For pre-sales: sign the developer's purchase agreement and pay your initial deposit — you get 7 days to rescind at no cost under REDMA.

Due Diligence Period

5-10 business daysThis is your subject removal window. Get the home inspected ($450-$800). Request the Form B Information Certificate and depreciation report from the strata corporation. Confirm financing with the lender. Review title documents with your lawyer. Everything happens in parallel — do not wait on one to start the next.

Subject Removal

Day of deadlineOnce you are satisfied with inspection results, strata docs, and financing confirmation, you remove subjects and the contract becomes legally binding. Your deposit — typically 5% of the purchase price — is due within 24 hours. After this point, walking away means losing your deposit and potentially facing a lawsuit.

Conveyancing & Mortgage Finalization

30-45 daysYour lawyer orders a title search, prepares transfer documents, and coordinates with the lender. You sign mortgage papers, arrange home insurance (required by your lender before closing), and set up utility transfers. Property transfer tax is calculated and paid at this stage.

Completion & Possession

1-2 days apartCompletion day: title transfers to your name and the seller receives funds. Possession day (usually the next business day): you pick up the keys from your realtor. Do a final walk-through to confirm everything matches the contract, check appliances, and document any issues before the seller is out of reach.

Sources: BCFSA Home Buyer Rescission Period regulation (Jan 2023). Bank of Canada overnight rate decision (Mar 18, 2026). Ratehub.ca insured mortgage rates (Mar 2026). People's Law School BC home buying guide.

Real Closing Costs on a $900K Multiplex

This is what the bill actually looks like beyond your down payment. Budget 1.5-4% of the purchase price for closing costs — on a $900K multiplex, that means roughly $20,000-$25,000 on top of your down payment.

| Cost Item | Typical Range | On $900K Purchase | Notes |

|---|---|---|---|

| Property Transfer Tax | 1-2% of price | $16,000 | 1% on first $200K + 2% on $200K-$2M. First-time exemption caps at $860K. |

| Legal / Notary Fees | $1,200-$2,000 | $1,500-$2,000 | Title transfer, mortgage registration, document review. |

| Home Inspection | $450-$800 | $500-$800 | Standard inspection. Add $150-$400 for sewer scope, radon, etc. |

| Appraisal | $300-$500 | $350-$500 | Lender may require one. Some lenders cover the cost. |

| Title Insurance | $200-$400 | $250-$350 | Protects against title fraud, survey errors, unknown liens. |

| Home Insurance | $1,200-$3,000/yr | $1,500-$2,500/yr | Required before closing. Multiplex rates vary by unit count. |

| CMHC Insurance (if <20% down) | 2.8-4.0% of mortgage | $23,400-$33,400 | Added to mortgage balance. 4% at 5% down; 2.8% at 15% down. |

| Strata Form B Certificate | $100-$200 | $100-$200 | Requested from strata corp. Must be provided within 7 days. |

| Property Tax Adjustment | Varies | $500-$3,000 | You reimburse the seller for any prepaid property taxes. |

Sources: BC Gov Property Transfer Tax rates (gov.bc.ca). CMHC mortgage loan insurance premium schedule (cmhc-schl.gc.ca). WOWA.ca closing costs calculator (2026). BC Real Estate Lawyers closing cost guide.

Property Transfer Tax, Explained

PTT is the single largest closing cost for most multiplex buyers in BC. The rates are progressive, and the exemptions have specific thresholds that can save you five figures — or cost you that much if you are just over the line.

On the first $200,000 of fair market value. That is $2,000 on every single purchase, no exceptions.

On the portion between $200,000 and $2,000,000. This is where most of your PTT bill lives. On a $900K purchase, this bracket alone costs $14,000.

On the portion over $2,000,000. Plus an additional 2% surcharge above $3,000,000. Rarely applies to multiplex units, but good to know.

PTT Exemptions That Actually Apply

Full exemption on properties up to $835,000. Partial exemption between $835K-$860K. Above $860K, nothing. You must be a Canadian citizen or permanent resident, have lived in BC for 12+ consecutive months, and never have owned a principal residence anywhere. On a $900K multiplex, you pay the full $16,000.

Full exemption on new builds up to $1,100,000. Partial exemption between $1.1M-$1.15M. Must move in within 92 days and live there for at least one year. This is the big one for multiplex buyers — most new-build units fall under this threshold. A $900K new-build multiplex unit means $0 PTT.

Sources: BC Gov Property Transfer Tax rates and exemptions (gov.bc.ca, effective April 1, 2024). First-time buyer and newly built home thresholds confirmed for 2025-2026.

Pre-Sale vs Resale: Side by Side

Most new multiplexes in Metro Vancouver sell pre-sale. That changes the buying process in ways that surprise first-timers — different deposits, different protections, different risks.

| Factor | Pre-Sale | Resale |

|---|---|---|

| Rescission Period | 7 days — free, no penalty (REDMA) | 3 business days — costs 0.25% of price (HBRP) |

| Deposit Structure | 15-25% paid in instalments over construction | 5% with offer, balance at completion |

| Move-In Timeline | 12-30 months (construction dependent) | 30-90 days after acceptance |

| GST (5%) | Yes — applies to all new builds | No — exempt on resale properties |

| Disclosure | Full disclosure statement required by law | Property Disclosure Statement (voluntary) |

| Customization | Choose finishes, upgrades, sometimes layout | What you see is what you get |

| Home Inspection | Deficiency walk-through before possession | Full inspection during subject period |

| Warranty | 2-5-10 year BC new home warranty (mandatory) | None, unless transferable from original build |

| PTT Exemption | Newly built: full exemption up to $1.1M | First-time buyer: full exemption up to $835K |

| Rate Risk | Rate hold may expire before completion | Lock in current rates, close in weeks |

| Developer Risk | Construction delays, spec changes, insolvency | None — the building already exists |

Sources: BCFSA presale disclosure requirements (bcfsa.ca). BC Real Estate Development Marketing Act (REDMA) rescission rules. BCFSA Home Buyer Rescission Period regulation (Jan 2023). BC Housing 2-5-10 new home warranty requirements. BC Gov newly built home PTT exemption (effective Apr 2024).

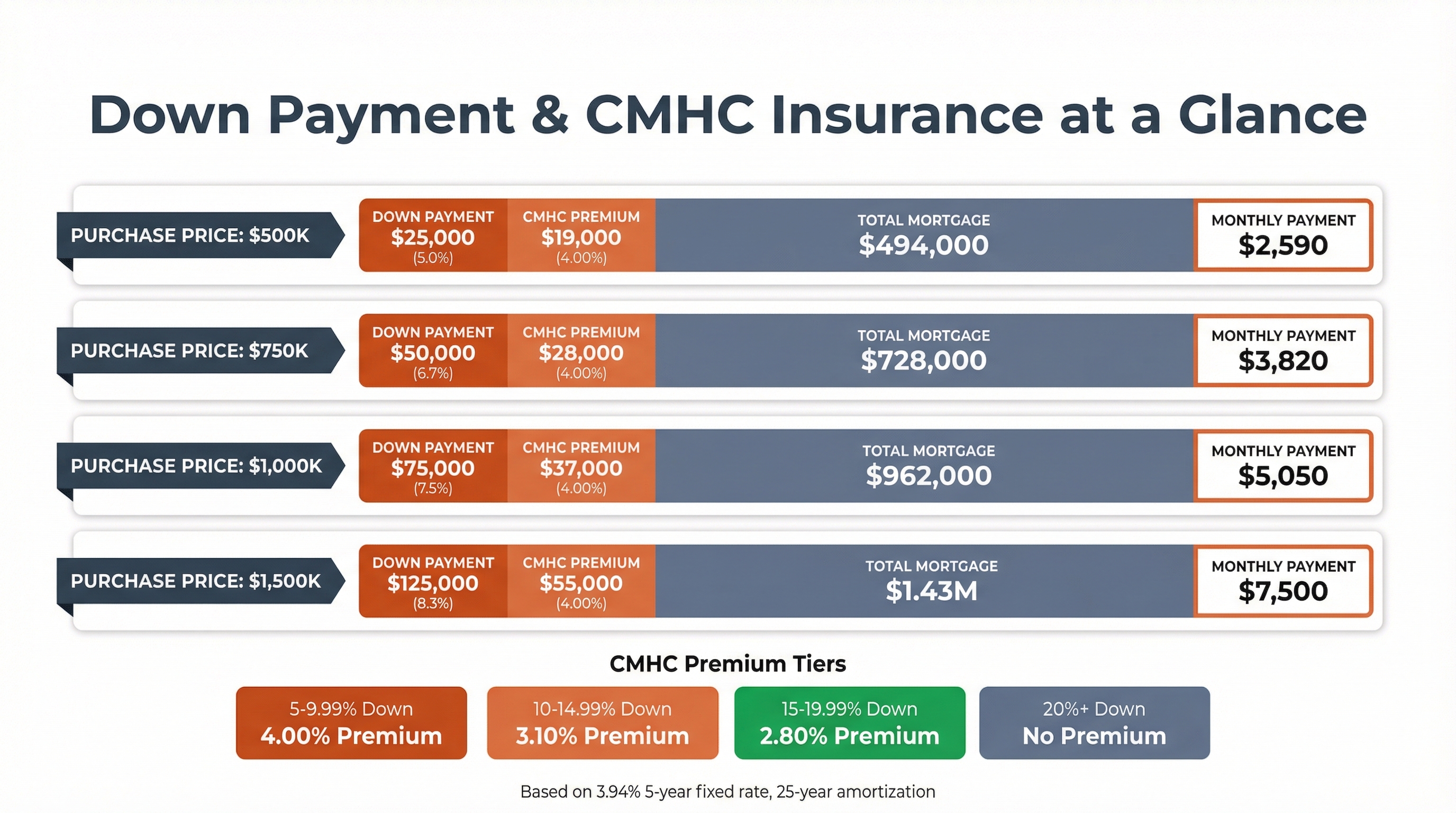

CMHC Premiums by Down Payment

Put down less than 20% and you pay mortgage default insurance. The premium gets added to your mortgage balance, so you pay interest on it for 25-30 years. Here is what that looks like on a $900K purchase.

Watch the minimum down payment math: On a $900K purchase, the minimum is $65,000 — not $45,000. CMHC rules require 5% on the first $500K ($25,000) plus 10% on the remaining $400K ($40,000). CMHC insures owner-occupied properties up to $1.5M since December 2024. First-time buyers on new builds qualify for 30-year amortization, which lowers monthly payments.

Sources: CMHC mortgage loan insurance premium schedule (cmhc-schl.gc.ca). CMHC insured mortgage rules update (Dec 15, 2024). Ratehub.ca CMHC insurance calculator (2026). Premium rates are identical across CMHC, Sagen, and Canada Guaranty.

Why Multiplex Ownership Is Different

Beyond the numbers, buyers who have made the move describe a set of benefits that don't show up in any spreadsheet. These are the reasons people don't regret it.

A Dynamic Living Arrangement

A multiplex is not a fixed product. Live in one unit and rent another today. Have an aging parent move in next year. Convert a rental unit to a home office suite when you need the space. The structure adapts to how your life actually changes — something a single condo unit never can.

Off the Bus Route, On a Real Street

Most new multiplexes are being built on quiet residential streets in established neighbourhoods — not on arterials beside bus stops and retail. You get neighbourhood character and walkability without the noise. This is one of the most consistent things buyers mention after moving from a downtown high-rise.

A Generational Housing Solution

No other housing type serves a growing family, multigenerational household, and future empty-nester all at once. A fourplex works when you need space for kids, works when parents move in, and works when you want rental income in retirement. You're not buying a house for right now — you're buying a structure that works for the next 30 years.

Real Neighbourhood Choice

Condo towers cluster in specific corridors — Brentwood, Marine Drive, Surrey Central. Multiplexes are distributed across dozens of Metro Vancouver neighbourhoods that never had new-build supply before Bill 44. Hastings-Sunrise, Renfrew, Collingwood, Burnaby Heights, Queensborough — the inventory is where established communities already are.

Holds Value in Established Areas

A well-located multiplex in an established neighbourhood — mature trees, good schools, transit within walking distance — has historically held value better than condos in new high-rise corridors that flood the market with similar units. Land value drives the floor. In Metro Vancouver, land doesn't go down for long.

More Configurations, Less Cookie-Cutter

A pre-sale condo in a 300-unit tower means your 2BR is one of 60 identical 2BRs in the building. A multiplex has 2–6 units — often with meaningful differences in size, layout, level, and outdoor space. Buyers choose a specific unit, not a unit type. The product is less commoditized, which shows up in both the buying experience and the resale.

The bottom line

Buyers who do the homework consistently find the numbers work better than expected. The ownership structure is more flexible than anything a condo tower offers, and the lifestyle — private entrance, outdoor space, neighbours you actually know — is exactly what most families are looking for.

The purchase process has a few more steps than buying a condo — Form B, depreciation report, subject removal — but each one is designed to give you clarity and confidence. A good real estate lawyer walks you through it in a few hours, and the information you gain (reserve fund health, pending special levies, bylaw restrictions) means you buy with eyes wide open.

The PTT math rewards you on new builds. A $950K pre-sale multiplex unit means zero PTT under the newly built home exemption — that's $17,000 saved at closing. Most new Bill 44 multiplexes fall comfortably under the $1.1M threshold. Add the 2-5-10 warranty on new construction — two years on labour and materials, five on the building envelope, ten on structure — and you're buying a BC Housing-certified building, not someone else's deferred maintenance.

The long game speaks for itself. Land in Metro Vancouver holds value over every 10-year cycle. A well-located multiplex in Renfrew, Mount Pleasant, or Burnaby Heights — established neighbourhoods with walkable amenities and transit access — builds equity on a foundation that appreciates. You own ground in one of the most supply-constrained markets in North America.

The process is manageable, the costs are knowable, and the upside is real. Bill 44 supply is here now and growing fast. Explore the full Playbook for more guides, or talk to our team and we'll match you with the right project.

Data: BC Gov PTT rates and exemptions (gov.bc.ca). BCFSA rescission period regulations. BC Housing 2-5-10 warranty requirements. Bank of Canada rate decision, March 18, 2026. CMHC insured mortgage rules (Dec 2024).

Key Takeaways

- New-build PTT exemption up to $1.1M saves $17K at closing — most Bill 44 multiplexes qualify.

- CMHC counts 50% of rental income toward qualification — transformative for fourplex buyers.

- 2-5-10 warranty on every new BC multiplex means zero deferred maintenance risk on day one.

- Resale closes in 60-90 days; pre-sale takes 18-24 months but locks in pricing and PTT exemption.

- Minimum down payment on $900K is $65K (5% on first $500K + 10% on remainder) — not $45K.

- The 7-day pre-sale rescission is free; the 3-day resale rescission costs 0.25% of price.

Frequently Asked Questions

How long does it take to buy a multiplex in BC?

A resale multiplex purchase typically takes 60-90 days from accepted offer to possession. Pre-sale purchases lock in the price immediately but require 12-30 months for construction before you can move in. The subject removal period is usually 5-10 business days.

The timeline breaks down roughly as follows for resale: 1-2 weeks for mortgage pre-approval, 2-8 weeks of active searching, then once you have an accepted offer, 5-10 business days for subject removal (inspection, financing confirmation, title review), and 30-60 days to completion. Pre-sale is a different animal — you sign a contract of purchase and sale, pay deposits in stages over the construction period, and wait for the developer to finish building. Construction timelines in Metro Vancouver have been running 12-30 months depending on project complexity. During that waiting period your deposit is held in trust. Budget for the possibility of construction delays, which are common and can push your move-in date back by several months.

What is the Property Transfer Tax in BC?

BC charges 1% on the first $200K of fair market value and 2% on $200K-$2M. On a $900K resale multiplex, that is $16,000. New builds are fully exempt up to $1.1M under the newly built home exemption, and first-time buyers are exempt up to $835K on resale.

Property Transfer Tax is one of the biggest closing costs that catches buyers off guard. On a $900K resale unit, you are looking at $16,000 due on completion day — and it cannot be rolled into your mortgage. First-time buyers purchasing resale should check if they qualify for the full or partial exemption (full exemption up to $835K, partial up to $860K). If you are buying a new build, the newly built home exemption covers properties up to $1.1M with a partial exemption up to $1.15M, regardless of whether you are a first-time buyer. Your notary or lawyer will calculate the exact amount during the closing process. Factor this into your cash-on-hand planning alongside legal fees, inspection costs, and moving expenses.

Do I need a home inspection for a multiplex?

Yes. A standard home inspection in Metro Vancouver costs $450-$800. For resale multiplexes, schedule it during the subject removal window. For new builds, you do a deficiency walk-through instead. Add $150-$400 for specialties like sewer scope or radon testing.

A home inspection is your best protection against costly surprises. For resale multiplexes, your inspector should check the building envelope, foundation, roof, plumbing, electrical, and HVAC systems — the same as any house, but with attention to shared walls and separate utility configurations. Book the inspection immediately after your offer is accepted so results come back within the subject removal window. For new builds covered by a 2-5-10 warranty, a formal home inspection is less critical, but a thorough deficiency walk-through before completion is essential. Bring a checklist and photograph everything. Consider hiring an independent inspector even for new builds — they often catch items that the developer's own quality team missed. Sewer scopes are particularly worthwhile on older lots where the lateral line may need replacement.

What's the difference between pre-sale and resale multiplex?

Pre-sale means buying before construction is complete — you get a 7-day free rescission period, GST applies (5%), and a mandatory 2-5-10 year warranty. Resale means the unit already exists — you get a 3-day rescission period (costs 0.25%), no GST, and no warranty unless transferable.

The choice between pre-sale and resale comes down to trade-offs. Pre-sale lets you lock in today's price and spread your deposit payments over the construction period, but you are buying based on floor plans and renderings — the finished product may differ from what you imagined. You also pay 5% GST on the purchase price, though owner-occupiers can claim back up to $6,300 via the federal GST New Housing Rebate. Resale means you walk through the actual unit, see the finishes, meet the neighbours, and move in within weeks. But there is no warranty unless the original 2-5-10 coverage is still active and transferable. The 3-day rescission period on resale costs 0.25% of the purchase price if exercised, compared to the free 7-day window on pre-sale.

Should I buy pre-sale or wait for resale multiplexes?

Pre-sale locks in today's price with a 15-20% deposit spread over construction, but you pay 5% GST and wait 12-30 months. Resale lets you inspect the actual unit and move in within weeks, but no GST rebate and fewer options on the market right now.

This is genuinely a toss-up and depends on your timeline. Pre-sale advantages: you secure current pricing, get a 7-day free rescission period under REDMA, and can claim up to $6,300 back via the GST New Housing Rebate as an owner-occupier. Pre-sale risks: construction delays are common in Metro Vancouver, the finished unit may not match the showroom, and your deposit is tied up for over a year. Resale advantages: you walk through the real unit, see the actual finishes, check the sound insulation yourself, and close in 60-90 days. Resale risks: fewer multiplex units exist on the resale market since most Bill 44 projects are still under construction, and you lose the 2-5-10 warranty coverage unless it transfers. Our take: if you need to move within six months, resale is your only option. If you can wait and want to lock in pricing during a soft market, pre-sale gives you more negotiating leverage right now.

What happens if the developer goes bankrupt before completion?

Your deposit is protected under BC's Real Estate Development Marketing Act (REDMA), which requires developers to hold deposits in trust. The 2-5-10 home warranty from BC Housing also provides structural coverage even if the builder disappears.

REDMA is your first line of defence. All pre-sale deposits must be held in a lawyer's or notary's trust account — the developer cannot touch them during construction. If the developer goes under, your deposit is returned from trust. That said, you lose the time you waited and any price appreciation you expected. The 2-5-10 warranty through BC Housing covers 2 years on labour and materials, 5 years on the building envelope, and 10 years on structural defects. This warranty follows the building, not the builder, so it survives a bankruptcy. What is not covered: any upgrades or customizations you negotiated, appliance choices, or completion timeline guarantees. To protect yourself, research the developer's track record before signing. Check BC Housing's licensing database, look at their previous projects, and ask your realtor about their financial stability. If a deal seems too good to be true during pre-sale, there may be a reason.

Buying Articles

Pre-Sale Buyer's Checklist

REDMA rules, deposit protection, risk assessment, and what pre-sale buyers wish they knew.

Multiplex vs Half-Duplex

Definitions, strata governance differences, and which structure fits your situation.

Multiplex vs Condo vs Townhouse

Side-by-side comparison with real pricing, monthly costs, and who should buy what.

Co-Development Explained

Partner with a developer to build a multiplex on your lot — deal structures, timelines, costs, and risks.

More from The Playbook

Why Multiplex

The case for ground-oriented living

ExploreFinancing

Mortgages, programs & more

ExploreMarket Reports

Data, trends & analysis

ExploreLiving

What ownership looks like

ExploreMulti-Gen

Families buying together

ExploreWhere to Buy (Van)

Vancouver neighbourhood data

ExploreWhere to Buy (Burnaby)

Burnaby neighbourhood data

ExploreTalk to a Multiplex Expert

Whether you're buying, building, or exploring your options — our team can help you navigate the process with confidence.

Ready to find your multiplex?

Browse duplexes, triplexes, and fourplexes across Greater Vancouver and BC.