Multiplex Investment Returns & Cash Flow

Metro Vancouver cap rates for multifamily sit around 4.7%, gross yields run 4.5-5.2% on a well-located fourplex, and the vacancy rate just hit 3.7% -- the highest since 1988. Here's what the numbers actually look like when you own one.

Key Topics

Cap Rates Are Climbing

Suburban multifamily cap rates in Metro Vancouver rose to 4.66% in 2025, up from the sub-4% levels of 2022-2023. Higher rates mean lower asset prices relative to income -- which is actually good news for buyers entering the market now.

Gross Yields of 4.5-5.2%

A $1.2M fourplex generating $4,500-$5,200/month in rental income (owner-occupying one unit, renting three) delivers gross yields in the 4.5-5.2% range. That's before expenses -- but it's a real starting point for the math.

Operating Costs: 35-45% of Rent

Property taxes, insurance, maintenance, and vacancy allowance eat 35-45% of gross rental income on a small multifamily building. For a fourplex, budget $1,500-$2,200/month in total operating expenses before mortgage payments.

Multiplex vs. Condo Returns

Condos in Metro Vancouver yield roughly 3.2% gross. A fourplex with rental suites can push 4.5-5.2%. The per-square-foot cost is lower, the income is higher, and attached homes lost only 3.8% in 2025 versus 5.3% for condos.

Owner-Occupier Advantage

Living in one unit and renting three means you qualify for CMHC-insured financing at 5% down (up to $1.5M). Lenders count 50% of projected rental income for qualification, boosting your purchasing power by $100K or more.

5-Year Appreciation Story

Detached home benchmarks dropped 5.3% in 2025, but the 10-year compound appreciation for Metro Vancouver residential property has averaged 5-7% annually. Multiplexes on land benefit from both rental income and long-run lot value growth.

Fourplex Proforma: $1.2M Purchase

Owner-occupied fourplex in East Vancouver. You live in one unit, rent three. Here's what the first year looks like.

| Line Item | Monthly | Annual |

|---|---|---|

| Income | ||

| Rental income (3 units x $2,500 avg.) | $7,500 | $90,000 |

| Less vacancy allowance (5%) | -$375 | -$4,500 |

| Effective Gross Income | $7,125 | $85,500 |

| Operating Expenses | ||

| Property taxes | $340 | $4,080 |

| Insurance | $310 | $3,720 |

| Maintenance reserve (1% of value) | $1,000 | $12,000 |

| Common utilities | $250 | $3,000 |

| Strata / admin | $200 | $2,400 |

| Total Operating Expenses | $2,100 | $25,200 |

| Debt Service | ||

| Mortgage ($1.105M @ 3.9%, 25yr amort.) | $5,100 | $61,200 |

| CMHC premium (amortized) | Included | Included |

| Net Cash Flow (before you live rent-free) | -$75 | -$900 |

Translation: You're roughly break-even on cash flow -- paying about $75/month out of pocket for a place to live, while tenants cover the rest. Compare that to renting a 2BR in Vancouver at $2,363/month. Your effective housing cost dropped by 97%. And you're building equity with every mortgage payment.

Assumptions: $1.2M purchase, $95K down (CMHC-insured), 3.9% 5-year fixed rate (March 2026), 25-year amortization. Rental income at $2,500/unit avg. -- between CMHC purpose-built avg. ($2,363) and asking rents ($3,170). Sources: CMHC Rental Market Report Oct 2025, Ratehub.ca March 2026, City of Vancouver tax rates 2025.

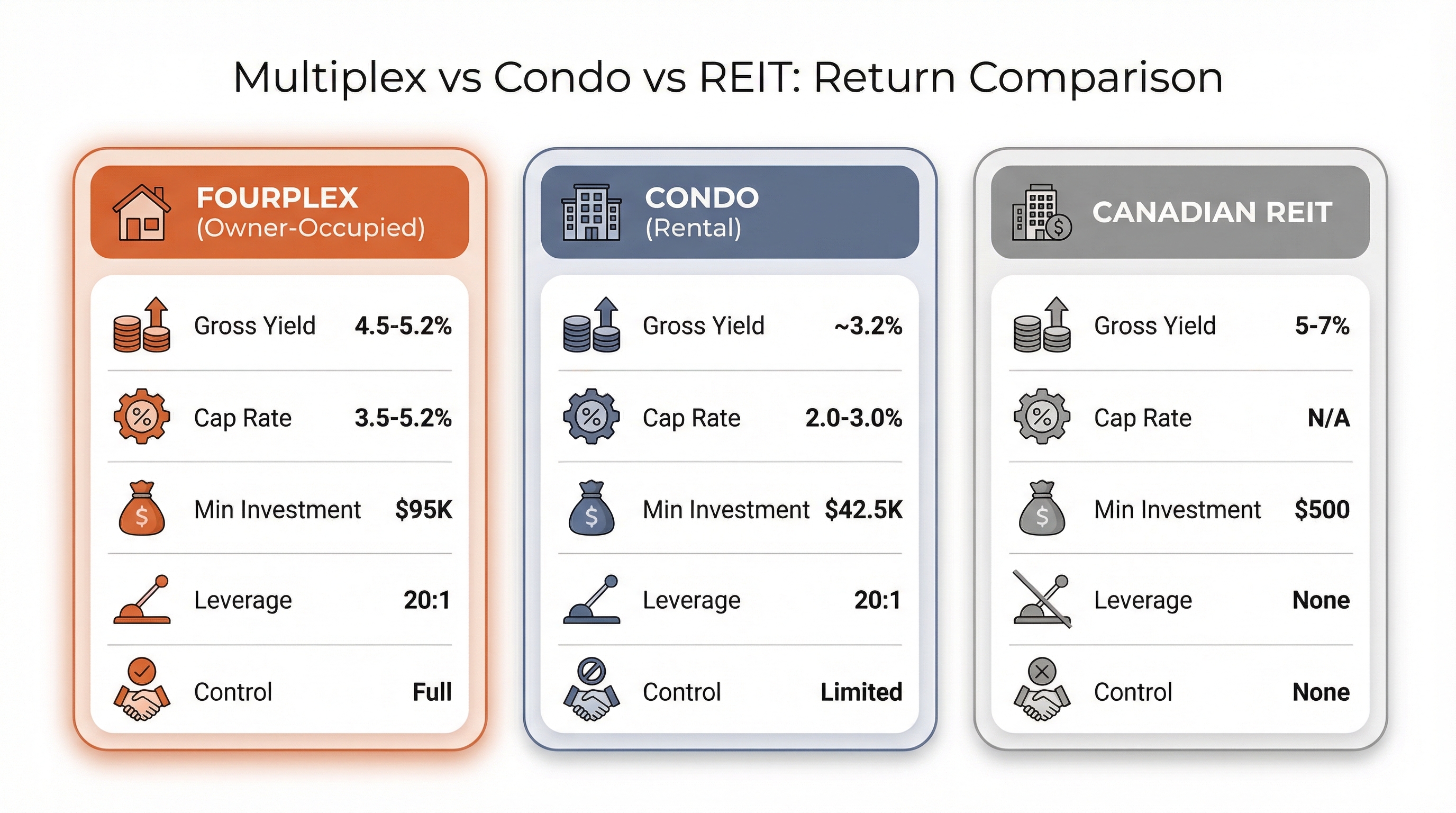

Multiplex vs. Condo vs. REIT

Three ways to put money into real estate in BC. Different risk, different liquidity, very different control.

| Metric | Fourplex (Owner-Occ.) | Condo (Rental) | Canadian REIT |

|---|---|---|---|

| Gross Yield | 4.5–5.2% | ~3.2% | 5–7% (distribution) |

| Cap Rate | 3.5–5.2% | 2.0–3.0% | N/A (market-priced) |

| Cash-on-Cash (Year 1) | -1% to 2% | -3% to -1% | 5–7% |

| Appreciation (2025 YoY) | -3.8% (attached) | -5.3% (condo) | Varies by fund |

| 10-Year Avg. Appreciation | 5–7%/yr | 4–6%/yr | 3–5%/yr (total return ~8%) |

| Minimum Investment | $95K (5% down) | $42.5K (5% down) | $500 (TSX-listed) |

| Leverage | Up to 20:1 (CMHC) | Up to 20:1 (CMHC) | None typical |

| Liquidity | Low (months to sell) | Low (months to sell) | High (sell same day) |

| Tax Shelter | CCA + expense deductions | CCA + expenses | Distributions taxed |

| Control | Full (you manage it) | Limited (strata rules) | None |

Sources: REBGV MLS HPI Dec 2025, CMHC Rental Market Report Oct 2025, Global Property Guide Vancouver yields 2025, S&P/TSX Capped REIT Index. Appreciation figures are Metro Vancouver benchmarks.

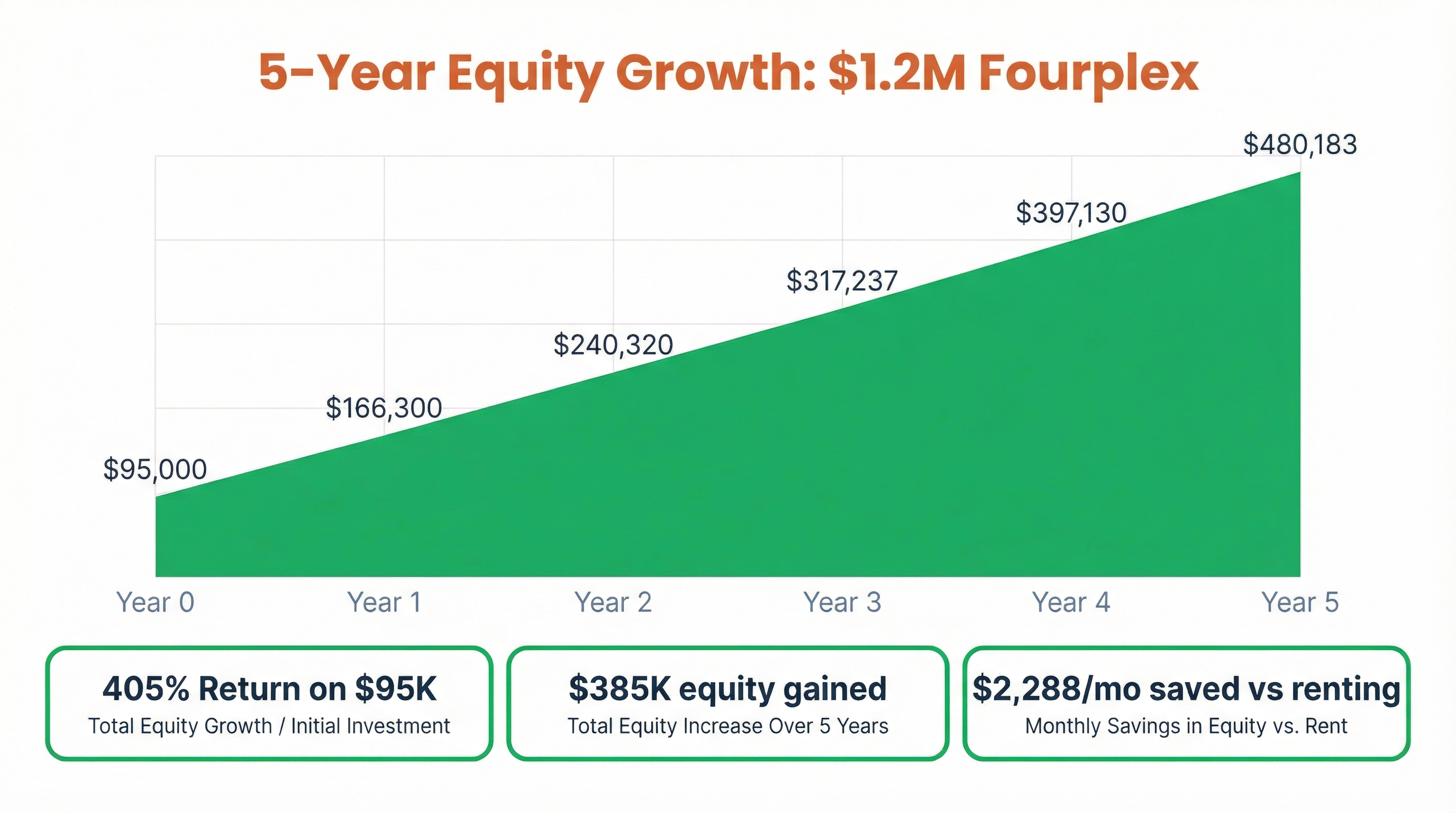

5-Year Projection: $1.2M Fourplex

Conservative scenario: 3% annual rent growth (BC CPI cap), 4% annual appreciation, 5% vacancy. No renovations, no refinancing.

| Year | Property Value | Annual Gross Rent | Annual NOI | Mortgage Balance | Total Equity |

|---|---|---|---|---|---|

| 0 | $1,200,000 | — | — | $1,105,000 | $95,000 |

| 1 | $1,248,000 | $85,500 | $60,300 | $1,081,700 | $166,300 |

| 2 | $1,297,920 | $88,065 | $62,109 | $1,057,600 | $240,320 |

| 3 | $1,349,837 | $90,707 | $63,985 | $1,032,600 | $317,237 |

| 4 | $1,403,830 | $93,428 | $65,930 | $1,006,700 | $397,130 |

| 5 | $1,459,983 | $96,231 | $67,947 | $979,800 | $480,183 |

Projection assumes 4% annual appreciation (below Metro Vancouver 10-year average of 5-7%), 3% annual rent increases (BC CPI cap), and constant operating expense ratio of ~29% of gross income. Mortgage paydown calculated at 3.9% 5-year fixed, 25-year amortization. This is a model, not a guarantee.

Operating Expense Breakdown

Annual costs for a $1.2M fourplex in Vancouver. These numbers eat into your gross yield -- and most projections underestimate them.

Property Taxes

$4,080Vancouver residential rate: $3.12 per $1,000 assessed value. Burnaby and Surrey run slightly lower.

Insurance

$3,720Four-unit wood-frame building. Includes liability, fire, and loss of rental income coverage. Rates rose 8-12% in 2024-2025.

Maintenance Reserve

$12,000Industry rule: 1% of property value per year. Covers appliance replacement, plumbing, painting, and the occasional emergency. New builds need less; older conversions need more.

Common Utilities

$3,000Shared water, garbage, and common-area electricity. Individual unit heat and power are typically tenant-paid in newer multiplexes.

Vacancy Allowance

$4,5005% of gross rent. With Metro Vancouver vacancy at 3.7% and climbing, this is the minimum buffer. Some years you'll use it, some you won't.

Property Management

$0–$7,2008% of collected rent if you hire a manager. Most owner-occupiers self-manage and keep this at $0. Your time has value though -- don't forget that.

That's 29.5% of gross rental income -- below the industry benchmark of 35-45% because you're self-managing. Add a property manager and you're at 37-38%.

Sources: City of Vancouver residential tax rates 2025, CMHC Rental Market Report Oct 2025, industry benchmarks from Baselane and Stessa rental expense guides.

What the Internet Gets Wrong

"You'll cash flow $3,000/month from day one"

At current prices and rates, a $1.2M fourplex with 5% down is roughly break-even on cash flow in year one. The real return comes from living rent-free, building equity, and long-term appreciation. Anyone promising instant cash flow at Vancouver prices hasn't run the numbers.

"Cap rates don't matter in Vancouver -- it's all appreciation"

Prices dropped 3.8-5.3% across all property types in 2025. Betting purely on appreciation without positive cash flow is how people get into trouble. Cap rates matter because they tell you whether the property can survive a flat market.

"Vacancy is basically zero in Vancouver"

It was 0.9% in 2019. It's 3.7% now. That's a 4x increase in five years. Metro Vancouver added record rental supply in 2025, and population growth slowed sharply due to lower international migration. Budget 5% vacancy minimum.

"Just Airbnb the extra units for way more money"

Vancouver's Short-Term Rental Accommodation By-law requires you to live in the dwelling and limits STRs to your principal residence. You can't legally Airbnb a separate unit in your fourplex. The city fines violators up to $1,000/day.

Sources: CMHC Rental Market Report Oct 2025, REBGV MLS HPI Dec 2025, City of Vancouver STR By-law.

The bottom line

A fourplex in Metro Vancouver is a wealth-building engine, not a passive income play. With a $1.2M purchase, 5% down, and a 3.9% mortgage rate, you're roughly break-even in year one — and that's the point. You're living for nearly free while tenants build your equity. After five years, you're sitting on roughly $480K in equity from a $95K investment. That's leveraged wealth building with a roof over your head.

The real comparison is multiplex vs. renting at $2,363/month while saving for a detached home that costs $1.88M. An owner-occupied fourplex gives you a realistic path into the market — one that pencils out even with conservative assumptions. Today's softer market, with vacancy at 3.7% and rents stabilizing, actually gives buyers more negotiating room on purchase price.

Smart buyers model conservatively — modest appreciation, realistic vacancy, real maintenance costs. When you run those numbers honestly, multiplex ownership still outperforms renting and still beats trying to save your way into a detached home. The math works for buyers who have $95K–$120K saved and are ready to take an active role in building their financial future.

If you're weighing the numbers and want help making sense of what works for your situation, talk to our team. We help buyers find the right multiplex at the right price — and we know what the numbers actually look like on the ground. For a deeper dive into every step of the process, explore our Playbook.

Data: CMHC Rental Market Report Oct 2025, REBGV MLS HPI Dec 2025, Ratehub.ca March 2026, VanPlex market analysis, City of Vancouver tax rates.

Key Takeaways

- Suburban multifamily cap rates in Metro Vancouver reached 4.66% in 2025 -- up from sub-4%.

- A $1.2M fourplex can generate $54,000-$62,400/year in gross rental income from three units.

- Operating expenses run 35-45% of gross rent -- budget $18,000-$26,400/year for a fourplex.

- Vacancy hit 3.7% in Metro Vancouver -- build a 5% vacancy allowance into every projection.

- Attached homes declined only 3.8% in 2025, outperforming both condos (-5.3%) and detached (-5.3%).

- Owner-occupiers get CMHC insurance at 5% down, with 50% of rental income counting for qualification.

Frequently Asked Questions

What is a good cap rate for a multiplex in Vancouver?

Suburban multifamily cap rates in Metro Vancouver hit 4.66% in 2025, up from sub-4% in 2022-2023. For a buyer-occupied fourplex, effective cap rates range from 3.5% to 5.2% depending on location, with East Vancouver and Burnaby offering the strongest yields.

Cap rate is net operating income divided by purchase price. On a $1.2M fourplex generating $62,400 in gross annual rent from three units, with $24,960 in operating expenses (40%), your NOI is $37,440 -- a 3.1% cap rate. That looks thin, but it excludes the value of living rent-free in the fourth unit. If you add an imputed rent of $2,200/month ($26,400/year) for the unit you occupy, the effective return on your asset is closer to 5.3%. Cap rates have been climbing because asset prices softened while rents held relatively steady. For investors, the important comparison is against the 5-year fixed mortgage rate of around 3.9% -- positive leverage means your cap rate exceeds your borrowing cost, and at 4.66% suburban cap rates, that math currently works.

How much rental income does a fourplex generate in Vancouver?

A fourplex with three rented units in Metro Vancouver can generate $7,000-$9,000 per month in gross rental income, based on CMHC 2025 data showing average 2BR purpose-built rents of $2,363 and asking rents for new listings at $3,170 for a two-bedroom.

The income depends on unit configuration and location. Three 2-bedroom units at current purpose-built averages ($2,363 each) produce $7,089/month or $85,068 annually. At market asking rents for new listings ($3,170 each), that jumps to $9,510/month or $114,120 annually. Reality usually falls between these numbers -- your first tenants will pay closer to asking rent, but turnover rents normalize over time. For East Vancouver fourplexes with a mix of 1BR and 2BR suites, $7,500-$8,500/month is a realistic gross income target. Budget 5% vacancy ($375-$425/month) based on the current 3.7% Metro Vancouver vacancy rate, plus a small buffer. Also factor in that BC rent increase caps limit annual raises for existing tenants to CPI -- about 3% in recent years.

Is a multiplex a better investment than a condo in Vancouver?

On a pure yield basis, yes. Multiplex gross yields run 4.5-5.2% versus roughly 3.2% for condos. Attached homes also held value better in 2025, declining 3.8% compared to 5.3% for condos and 5.3% for detached, according to REBGV benchmarks.

Run the comparison on a $850K condo versus a $1.2M fourplex (owner-occupied). The condo at 600 sqft generates zero rental income and carries $450/month in strata fees. The fourplex generates $7,000-$9,000/month in gross rent from three units, with operating costs of $1,500-$2,200/month. After expenses, the fourplex nets $4,800-$7,500/month before mortgage -- the condo nets negative $450. Your mortgage payment is higher on the fourplex ($5,100/month at 3.9% on $1.14M), but the rental income covers most of it. The trade-off: you need a larger down payment ($60K minimum at 5% CMHC-insured versus $42.5K for the condo), and you take on landlord responsibilities. Over five years, the fourplex buyer builds equity faster through both appreciation and principal paydown subsidized by tenants.

What are the operating expenses for a multiplex in BC?

Operating expenses on a small multifamily building in Metro Vancouver typically run 35-45% of gross rental income. For a fourplex generating $85,000-$100,000/year in gross rent, expect $30,000-$45,000/year in property taxes, insurance, maintenance, and vacancy costs.

Here is a realistic breakdown for a $1.2M fourplex in Vancouver. Property taxes: $3,700-$4,200/year (Vancouver's residential rate is $3.12 per $1,000 of assessed value). Insurance: $3,000-$4,500/year for a four-unit wood-frame building. Maintenance and repairs: budget 1% of property value annually, so $12,000/year or $1,000/month. Property management (if you hire someone): 8% of collected rent, or $6,800-$8,000/year. Vacancy allowance at 5%: $4,250-$5,000/year. Utilities (if owner-paid): $2,400-$3,600/year for common areas. That totals $32,150-$37,300 in a typical year -- about 38-44% of gross income. The biggest variable is maintenance: a roof replacement or plumbing issue in year three can blow up your projections. Keep a $10,000 reserve fund and add to it monthly.

What is the vacancy rate for rental units in Vancouver?

Metro Vancouver's purpose-built rental vacancy rate hit 3.7% in October 2025, the highest since 1988, according to CMHC. This was driven by record new rental supply and reduced population growth from lower international migration.

The vacancy rate more than doubled from 1.6% in 2024 to 3.7% in 2025. For multiplex owners, this means two things. First, budget conservatively -- a 5% vacancy allowance is prudent given the upward trend. Second, landlords now compete for tenants. CMHC reported that purpose-built operators started offering incentives like a month of free rent and moving allowances. Average 2BR rents in Vancouver dropped to $2,363 -- the lowest same-sample rent growth in 20 years. The silver lining for owner-occupiers: you are not speculating on 100% occupancy. If you live in one unit and rent three, even one month vacant across all three units in a year only costs you $2,300-$3,200 in lost income. The owner-occupier model is inherently more resilient than a pure investment play.

How much down payment do you need for a fourplex in BC?

If you owner-occupy one unit, CMHC insures properties up to $1.5M with as little as 5% down on the first $500K and 10% on the remainder. On a $1.2M fourplex, that is a minimum down payment of $95,000.

The math works like this: 5% on the first $500K ($25,000) plus 10% on the remaining $700K ($70,000) equals $95,000 total. You will also pay a CMHC insurance premium of 4% on the loan amount ($44,200), which gets added to the mortgage. For a non-owner-occupied fourplex, you need 20% down ($240,000) and no CMHC insurance is available. First-time buyers on new builds can access 30-year amortization, which drops monthly payments by roughly $300 compared to the standard 25-year term. One important note: most lenders will count 50% of projected rental income from the other three units toward your mortgage qualification. On three units at $2,363/month each, that is $3,545/month in qualifying income -- enough to boost your purchasing power by $150,000 or more.

More from The Playbook

Why Multiplex

The case for ground-oriented living

ExploreBuying Guide

From discovery to closing

ExploreFinancing

Mortgages, programs & more

ExploreMarket Reports

Data, trends & analysis

ExploreLiving

What ownership looks like

ExploreMulti-Gen

Families buying together

ExploreWhere to Buy (Van)

Vancouver neighbourhood data

ExploreWhere to Buy (Burnaby)

Burnaby neighbourhood data

ExploreTalk to a Multiplex Expert

Whether you're buying, building, or exploring your options — our team can help you navigate the process with confidence.

Ready to find your multiplex?

Browse duplexes, triplexes, and fourplexes across Greater Vancouver and BC.